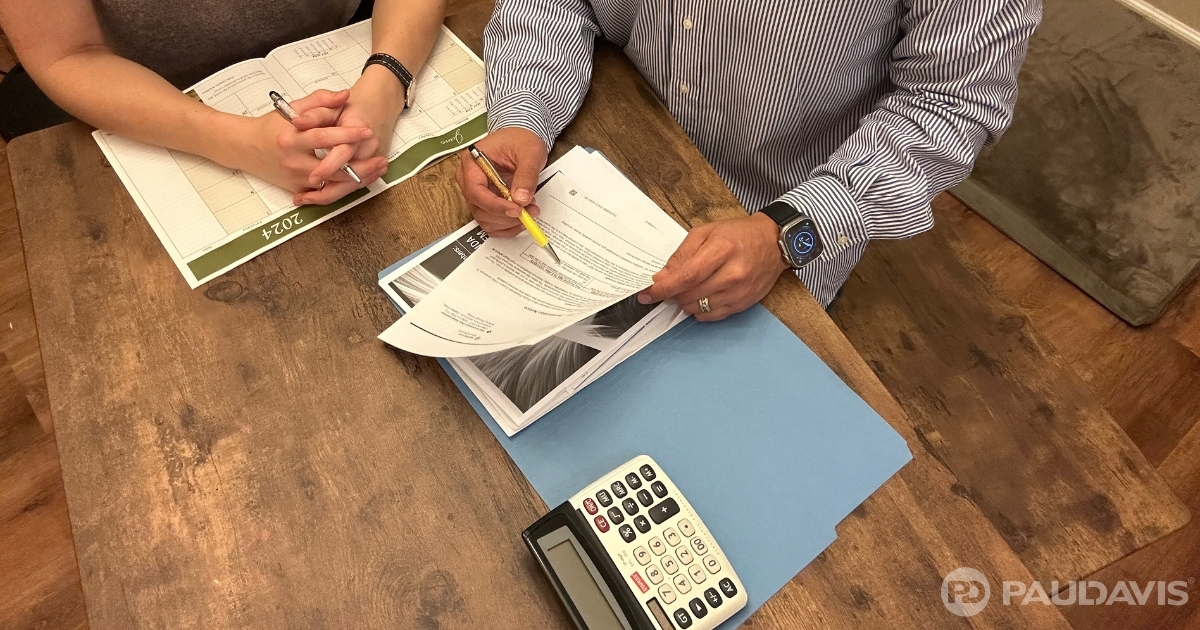

Higher prices are an exasperating reality and homeowner’s insurance is not exempt from sticker shock. “The average rise in homeowner’s policy cost last year was nearly nine percent. That’s good incentive to review your coverage as 2024 begins,” says Richard Green, President of Paul Davis Restoration Ottawa, Ontario.“Make an appointment with your insurance representative and come prepared with answers to a range of questions he or she will ask. Your goal is better economy and more comprehensive coverage.”

Every insurance broker or agent will review policy basics – company options for types and levels of coverage – but here are a few of the questions you might not anticipate:

Q: “Have you upgraded or downsized your home?”

Did you add a porch or other significant improvement? If so, expect an increase in coverage needs. Conversely, expect lower coverage requirements if you removed an existing structure or asset such as an outbuilding.

Q: Did you acquire or discard pricey possessions?

Homeowners policies protect personal property but optional coverages are needed for high-ticket items. List these items so your representative can evaluate if separate riders are needed to safeguard them. Conversely, getting rid of high value possessions may lower coverage costs.

Q: Did you start a home-based business?

Most homeowner’s policies don’t provide – or only provide a small amount – of home-based business coverage. Likely, a separate policy is the wise choice.

Q: Is your deductible right for you?

Canadian residents hit by recent storms are often shocked to discover how many expenses they shouldered because their deductibles were high. Ask your representative how your deductible amounts compare with potential losses, projected threats to your home, your current financial status, your plans for the property and the condition/age of your home.

Q: Are you comfortable with your coverage limits?

Every piece of coverage is subject to a maximum amount the carrier will pay out for a covered loss. Discuss each one with your representative. How much do you need to live elsewhere if your property becomes uninhabitable, for instance?

Q: Are you comfortable with liability coverage?

Typical policies provide liability protection if someone not living in your home injures themselves on your property. Do you own a pet? If so, inquire about coverage for pet damage and pet-caused injury. Do you need an umbrella policy to increase coverage?

Q: Do you need flood insurance?

As the climate changes, flood plain maps change, too. Ask your representative where your property stands in relation to updated flood threats.

“While you’re sitting down with your representative, consider changes in your family – life insurance may need revision or beneficiary changes – and car insurance,” Green says. “Almost every carrier offers significant monetary incentives to bundle all your policies with a single company.”